Navigating the world of projected interest rates in five years requires not only data-driven analysis but also context around the economic, political, and social dynamics shaping forecasts. As investors, homeowners, and business planners look ahead to 2029, understanding expert projections and their underlying assumptions is essential for risk management and strategic decision-making.

How Interest Rates are Forecasted

Forecasting future interest rates relies on a blend of economic modeling, market analysis, and policy assumptions. The U.S. Federal Reserve’s decisions act as a bellwether, influencing both short-term and long-term rates domestically and abroad.

Economic Indicators in Focus

Several key metrics shape rate projections:

- Inflation Trends: Central banks, including the Fed, target inflation (typically around 2%) as a primary mandate. Persistent inflation often pushes rates higher.

- Growth Outlook: GDP growth rates signal economic momentum. Strong growth can drive up rates, while recessions generally lead to cuts.

- Unemployment & Labor Markets: A tight labor market, often correlating with wage inflation, can spur rate hikes.

- Global Stability: Events like geopolitical tensions, energy crises, or pandemics can upend inflation and rate trajectories.

By synthesizing these indicators, economists develop scenarios that estimate where rates could land in five years. Still, uncertainty is the rule rather than the exception.

Expert Forecasts for Interest Rates in 2029

Federal Reserve and Major Central Banks

The Federal Reserve’s own Summary of Economic Projections (SEP), released quarterly, provides a valuable benchmark. As of early 2024, the consensus among Fed members suggested that the federal funds rate may moderate from recent highs but remain above pre-pandemic averages.

Many private sector and institutional forecasts (e.g., from the IMF, World Bank, and leading investment banks) align around the notion of a “higher-for-longer” environment. Recent years of stubborn inflation have challenged the idea of a swift return to the ultra-low rates of the 2010s.

“Most analysts agree that the era of near-zero interest rates is unlikely to return soon. Structural shifts in the global economy and persistent inflationary pressures are pushing forecasts for higher base rates deep into the decade.”

Beyond the U.S., central banks in Europe, Canada, and emerging markets are following similar—though not identical—paths, adjusting to local inflation and growth dynamics.

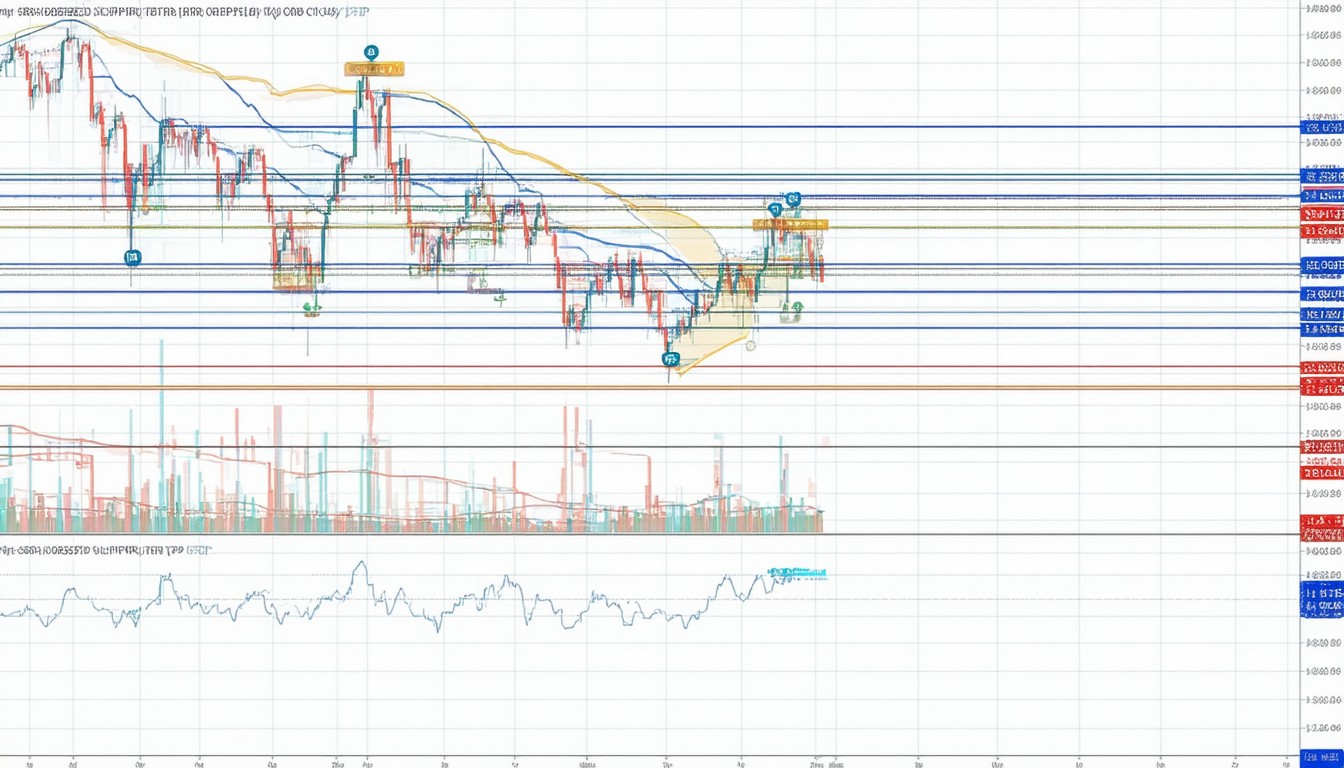

Market Implied Rates

Financial instruments like Treasury yields, Eurodollar futures, and interest rate swaps reflect market expectations for future rates. As of 2024, these assets price in moderate declines over the next two years, then relative stability or slight increases heading into 2029. This reflects both optimism about inflation control and caution about underlying risks.

For example, the 5-year U.S. Treasury yield—a real-time gauge of expectations—has hovered above its 2010s average, suggesting that markets foresee structurally higher rates in the medium term.

Drivers Influencing 5-Year Rate Projections

Inflation: Past, Present, and Prospects

Rising prices from 2021 through 2023 caught many forecasters off guard. Despite aggressive rate hikes in 2022–2023, inflation’s resilience exposed the limits of policy tools. While the consensus predicts moderating inflation, persistent wage growth and supply-side shocks could keep rates elevated.

Fiscal and Government Policy

Gigantic public spending during the pandemic—paired with new infrastructure and defense outlays—has increased government debt loads globally. Bond investors now demand higher yields to compensate for fiscal risks, a trend that could persist or intensify if deficits remain wide.

Global Shocks and De-Globalization

Recent years have seen a return of “geopolitical risk” as supply chains shift, nations reassess trade and energy partnerships, and political uncertainty clouds forecasts. These dynamics impact not only headline rates but also the volatility and risk premiums embedded in borrowed capital.

What a “Higher-for-Longer” Environment Means

Impact on Consumers and Borrowers

For homebuyers, mortgage rates closely track 10-year Treasury yields. Even modestly higher benchmark rates translate to significantly more expensive borrowing costs. Similarly, auto loans, credit cards, and student debt all become less affordable.

Businesses and Investment Strategy

Corporations face higher debt servicing costs, potentially stunting expansion or prompting more selective capital investments. Small businesses, in particular, may find accessing affordable credit more challenging.

Savers and Investors

On the upside, savers and holders of cash-equivalent instruments (CDs, money market funds) benefit from higher yields. For investors, bond pricing, equity valuations, and risk appetite all adjust to the new rate regime.

Key Scenarios: What Could Shift the Outlook?

While baseline forecasts suggest gradually declining rates, several “wild cards” could dramatically alter the 5-year trajectory:

- A Sharp Recession: A deep downturn could force central banks to cut rates aggressively, as seen in 2008 and 2020.

- Runaway Inflation: Supply chain shocks, energy crises, or persistent wage inflation could re-accelerate price growth, necessitating more hikes.

- Debt Crises: Fiscal instability, especially in emerging markets, could trigger both higher rates and wider credit spreads.

- Breakthroughs in Productivity: Technological leaps or demographic shifts could keep inflation low, enabling a return to easier money.

Real-World Examples: Comparing the U.S. and Europe

The U.S. historically leads rate cycles, given the dollar’s global role. By comparison, the European Central Bank (ECB) often lags the Fed, balancing different growth rates and inflation profiles across member countries.

For example, following the 2008 financial crisis, the Fed slashed rates rapidly and launched quantitative easing, while the ECB’s policy shifts were more gradual. In the 2020s, similar divergences could resurface if Europe’s inflation cools more quickly than the U.S., or if internal political dynamics force a change in course.

Strategic Considerations for the Next Five Years

For Borrowers

Locking in fixed-rate debt may provide a hedge against the possibility of rates staying structurally high. On the other hand, those expecting rates to fall sharply might prefer variable or adjustable-rate products, but this approach comes with greater risk.

For Investors

Asset allocation strategies need to account for both persistent rate volatility and the risk of structural shifts. Exposure to short-duration bonds, inflation-protected securities, or alternative assets may provide diversification benefits, though each comes with trade-offs.

For Policymakers

Central bankers and fiscal authorities must balance inflation control with growth and financial stability. Their ability to communicate policy intentions clearly—and to adjust flexibly to new data—will be key to managing expectations and containing surprises.

Summary: What to Watch Moving Forward

Forecasting the projected interest rates in 5 years is inherently uncertain, but several trends are clear. Persistently higher inflation, geopolitical instability, and fiscal pressures have shifted both expert and market expectations toward a “higher-for-longer” scenario. While rate cuts are possible if recession hits, most credible forecasts for 2029 see rates remaining above their 2010s lows.

Savvy consumers, investors, and business leaders must keep an eye on:

- Inflation data and central bank policy signals

- Fiscal trends and government debt sustainability

- Geopolitical developments and their market impact

Remaining flexible and informed is the best antidote to interest rate uncertainty.

FAQs

What are the most important factors affecting interest rate projections over five years?

Inflation, economic growth, government fiscal policy, global events, and central bank strategies are the primary factors. These all interact, making medium-term forecasts inherently uncertain.

Will mortgage rates be higher or lower five years from now?

Most forecasts suggest mortgage rates will remain higher than the ultra-low levels seen in the 2010s but could moderate somewhat from recent highs, depending on inflation and central bank action.

How do interest rate forecasts impact investment strategies?

Interest rate expectations shape bond yields, equity valuations, and the attractiveness of alternative assets. Investors often adjust their portfolios to reduce interest rate risk and seek yield that keeps pace with inflation.

Are variable-rate loans riskier in the current environment?

In a “higher-for-longer” scenario, variable-rate borrowers could see costs continue to climb. Locking in a fixed rate might be safer if sustained high rates are likely.

Could a recession cause rates to drop significantly?

Yes, a deep and sudden economic downturn could prompt central banks to cut rates rapidly, as they did during the 2008 financial crisis and the early stages of the COVID-19 pandemic. However, this is just one of several possible scenarios.